‘Hedge America’ Trade Fuels Global Rush Into Short-Dollar Wagers

(Bloomberg) — It turns out that all the “Sell America” angst swirling in markets earlier this year was misplaced.

The real mantra from global investors is more like “Hedge America” — that is, keep snapping up US stocks and bonds but do so while buying derivatives that protect those investments against any further declines in the dollar.

Most Read from Bloomberg

Starting around mid-year, and for the first time this decade, flows into dollar-hedged exchange-traded funds that buy US assets have outpaced those into unhedged funds, according to Deutsche Bank AG, which said the shift occurred at an unprecedented clip.

What it boils down to is that the notion of the exceptionalism of American markets, which seemed in jeopardy after President Donald Trump unveiled punishing global tariffs in April, is alive “with a twist” — avoiding exposure to the greenback, said Laura Cooper, a global investment strategist at Nuveen in London.

A sheet of $20 notes at the US Bureau of Engraving and Printing in Washington.Photographer: Al Drago/Bloomberg

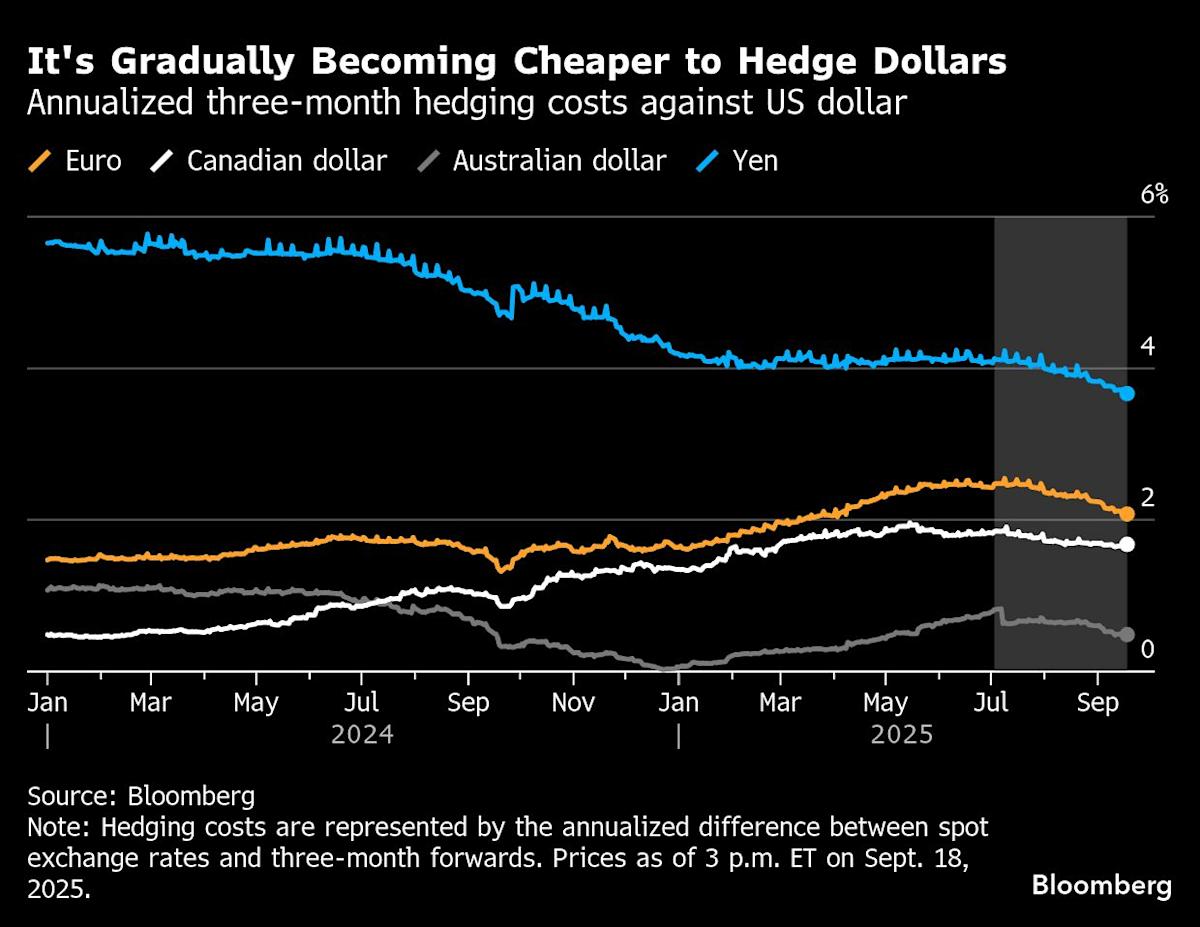

The hedging — which involves using derivatives to bet against the world’s primary reserve currency — helps explain why the dollar is teetering around its weakest level since 2022 even as US stocks have rallied. And now the prospect of more interest-rate cuts from the Federal Reserve is giving a jolt to the phenomenon, by making it cheaper for global investors to mitigate the currency risk that comes with investing in the US.

“My sense is the bulk of the adjustment is still ahead,” said Sahil Mahtani, director at Ninety One Asset Management’s Investment Institute in London.

$1 Trillion Wave

By Mahtani’s estimate, the wave of fresh dollar hedging could ultimately tally about $1 trillion. This would, he says, merely bring hedging levels from global investors, who own more than $30 trillion of US equities and bonds, back to where they stood last decade. That was before an appreciating dollar and the roaring stock market convinced many that they needed no protection.

Bloomberg’s gauge of the greenback fell to its lowest in more than three years this week. A chorus of banks including State Street Corp., Deutsche Bank, BNP Paribas SA and Societe Generale SA anticipate the hedging will weigh on the dollar heading into next year.

That pressure suggests that at the very least the currency will struggle to rebound from its roughly 9% slide in 2025, especially with the European Central Bank likely on hold for now. The Bank of Japan is expected to hike as soon as later this year.

One of the most popular hedging methods for foreign investors involves selling dollars forward to lock in exchange rates. It often translates into greater selling pressure on the dollar in the spot market. The cost of the transaction is largely a function of interest-rate differentials between the US and the other currency.

April Catalyst

The worries around the greenback, traditionally a haven for investors in times of crisis and economic stress, intensified after Trump’s tariff rollout in April. When stocks and US bonds tumbled, so did the dollar, suggesting that money managers were seeking shelter elsewhere, like in the Swiss franc, the euro and the yen.

Other US asset classes have rebounded since then, stocks in particular, but the dollar went on to its worst first-half performance since the 1970s. Hedging played into the slump. That activity by non-US investors was “an important contributor” to dollar weakness in April and May, the Bank for International Settlements has said.

For investors nervous that Trump is eroding the fundamentals underpinning a strong dollar, the concerns run far deeper than just tariffs. There’s also the president’s unprecedented campaign to remake the Fed board and his push to get it to rapidly cut rates; there’s his firing of a top government data collector after a jobs report he didn’t like; there’s his feuding with long-time foreign allies and even his growing crackdown on opposition groups and the media.

Steven Barrow, a strategist at Standard Bank in London, put it this way in a note to clients: “If there is speculation that the Fed is goosing the economy with rate cuts because of pressure from the White House, it would seem to make sense to love the US stock market and the front end of the Treasury market but to hate the dollar.”

Fresh evidence of that love of US bonds came Thursday, with government data showing foreign holdings of Treasuries rose to a record in July.

Overseas investors collectively own about $20 trillion of US stocks and some $14 trillion in US debt, including Treasuries, mortgage and corporate bonds. They’ve cut hedge ratios on US fixed income by some five percentage points and stocks by around two points in recent years, according to Ninety One Asset Management’s Mahtani, who cited academic research.

“Simply rewinding those modest moves would create roughly $1 trillion of dollar-selling FX trades,” he said.

Nailing down investors’ hedging activity precisely is tricky because of the challenge of tracking all the cash flowing around the world. Currency trading, for example, comes to about $7.5 trillion daily.

So estimates across Wall Street banks tend to vary. Data from State Street, one of the world’s largest custodian banks, shows a stabilization in hedging ratios on US assets held by foreign investors such as mutual funds, pension funds and insurers, after a decline from April levels. The ratio is now around 56%. For comparison, it was about 70% in mid-2023.

“Foreigners are unlikely to sell US assets — they are most likely to increase the hedge ratio,” said Lee Ferridge, a strategist at State Street. “The hedge ratio is crucial for the dollar story.”

Goldman Sachs Group Inc. analysts pointed out that the dollar started the year with high allocations and low hedge ratios — an unusual combination. Since then, there’s been an adjustment to that stance. “On net, data released so far show fairly consistent but relatively small shifts in FX hedge ratios from global pension funds,” the analysts wrote, pointing to reductions in unhedged exposure by Swedish, Danish and Finnish funds this year.

Unhedged Camp

Of course, money managers aren’t necessarily diving into hedging en masse.

“For our actively managed fixed-income products, we have not increased hedging positions against either currency risk or US Treasury yields,” said Ryan Chang, head of fixed income at Taipei-based CTBC Investments Co. The greenback is unlikely to fall sharply given a scenario of gradual Fed rate cuts, he said.

While there are signs of a pickup in hedging, for many investors it’s a process that plays out over years. But some big investors, such as pensions in Canada, Europe and Australia, have already signaled increases.

“We will be seeing a few more of these because investment committees have had time to look at this and to approve hedging programs,” said Alfonso Peccatiello, chief investment officer at Palinuro Capital in Amsterdam.

For Stephane Deo, senior portfolio manager at Eleva Capital in Paris, the move to hedge his US stock investments came at the start of the year.

The firm put on the hedge when the euro was trading at $1.05, near the weakest since late 2022. It has since appreciated to above $1.17, putting it among the Group-of-10 currencies that have logged double-digit gains against the greenback this year.

Part of Deo’s reasoning was that he expected the Trump administration to push for a weaker dollar. The firm had rotated heavily toward European stocks at the end of 2024 and shed exposure to US shares ahead of Trump’s April tariff announcement.

“We have since reinvested in the US,” he said. “So our dollar hedge is a position we intend to keep, as for the moment we expect the US stock market to rise along a weakening dollar.”

–With assistance from Julien Ponthus, Matthew Burgess, Ruth Carson, Vassilis Karamanis, Naomi Tajitsu, Stefani Reynolds, Alice Gledhill and Betty Hou.

Leave a Comment

Your email address will not be published. Required fields are marked *